Opening Statement of Commissioner Rostin Behnam before the Market Risk Advisory Committee

January 31, 2018

Introduction

Good morning and welcome to the first Market Risk Advisory Committee (“MRAC”) meeting of 2018. I am pleased to sponsor this Committee, and believe my timing to address important market risk issues could not be better. Ground-breaking new ideas have gone from theory to application in just the past few months. I am especially mindful and appreciative of the Commission’s ongoing efforts to affirmatively exercise its regulatory authority and expertise while remaining ever vigilant of the risks associated with the adoption of nascent technologies.

Before we move into the substance of today’s meeting, I want to thank Commissioner Quintenz and Chairman Giancarlo for being here today and for their contributions to this discussion.

I also want to thank today's moderator, Paul Architzel. Before entering private practice, Paul spent more than 25 years at the CFTC in the Office of General Counsel and as Chief Counsel in the CFTC’s former Division of Economic Analysis, now the Division of Market Oversight. Paul played a leading role in many rulemakings that shaped our current processes for new product review and approval. Since leaving the Commission in 2003, Paul has remained an active and well-respected member of the derivatives bar. Thank you, Paul, for facilitating our ambitious agenda.

I want to thank each of the panelists. We have gathered a distinguished group of speakers, and their readiness to participate is greatly appreciated and critical to today's discussion.

I want to thank Alicia Lewis, the Committee's Designated Federal Officer. Alicia started working in my office in mid-December, and MRAC was task number one on day one. She has handled the role with great professionalism and discipline, and the quality of her work will be displayed throughout the day.

I also want to thank the members of the MRAC. Today we welcome two new members, Jason Cohen, Chief Executive Officer of NEX SEF and Kathleen Cronin, Senior Managing Director and General Counsel of CME Group. Jason and Kathleen will be taking the place of departing MRAC members John Nixon and Kimberly Taylor. Former Commissioner Bowen selected this impressive group and you have all demonstrated the ability to tackle and opine on difficult and important issues. Your time and service is greatly appreciated.

However, as you may know, the charter for this Committee will expire in the next few months. Today will likely be the last meeting of this group before we renew the charter and reconstitute membership.

Why Now?

As I recently stepped into my role as the Sponsor of this Committee, it perhaps would have been sensible to renew, re-populate, and set a new course for the MRAC all at once. However, the introduction of two Bitcoin futures contracts caused many to inquire about—perhaps for the first time—the Commission’s role in the listing of new products under the Commodity Exchange Act (the “CEA” or “Act”) and Commission regulations.

While I commend the Chairman for releasing backgrounders on self-certification of bitcoin products and on the oversight of and approach to virtual currency futures markets,1 recording a podcast roundtable with CFTC leaders on Bitcoin,2 and launching a Bitcoin education webpage,3 these communications can fall flat in the absence of meaningful dialogue.

The launch of the Bitcoin futures products is a testament to the forward thinking, innovative spirit of the derivatives markets. As the market and market participants continue to adopt technologies that make new products, new relationships, and new forms of conduct possible, I believe it is critical that the CFTC: (1) engage with industry in addressing risk; (2) provide legal and regulatory certainty to the market; (3) educate the general public; and (4) question and challenge the status quo, in the market and within the Commission.

A Question of Process

Turning to today’s agenda, the four panels are organized and ordered to ensure our dialogue remains focused on the issue of self-certification of new products. That being said, in thinking about this meeting, and the Commission’s recently announced approach and responsibilities with respect to virtual currencies—unquestionably new and novel assets—the overarching theme is largely one of process. We all should feel accountable for what we do, but also for what we do not do. And while we are now living in an age that is not big on process, but often prefers to emphasize “likes” and tweetable sound bites, process is important because it provides the bearings, the connections in the record—and in the story—of how we accomplish our duties.

By way of background, the Commodity Exchange Act and the Commission regulations, Parts 40.2 and 40.3 specifically, provide for two processes when it comes to the listing of a new contract (or other instrument) for trading by a designated contract market (“DCM”) or swap execution facility (“SEF”)4, which I’ll refer to together as “exchanges”. Generally, under the Act, an exchange may either elect to list a new product for trading under Regulation 40.2 through written certification that the new contract complies with the Act and Commission regulations, or it may request that the Commission grant prior approval for the listing of the new contract under Regulation 40.3.5 If an exchange requests approval under Regulation 40.3, the Commission then must approve the new contract, unless it finds that the contract would violate the Act or Commission regulations.6 Regulations 40.2 and 40.3 implement these processes, setting forth, among other things, the contents of required submissions, the Commission’s authority to stay the listing of new products, the Commission’s authority to request—and the duty of the exchange to provide—additional information, and the applicable timelines.7

Relevant to today’s discussion, for self-certification, the exchange must file its submission with the Commission “by the open of business on the business day preceding the product’s listing.”8 This timeline reflects the Commission’s reliance on the exchanges, which have clear incentives to list contracts that comply with the Act and will not be susceptible to manipulation; and which have well-developed, sophisticated surveillance and self-regulatory systems. This timeline also reflects the understanding that the self-certification process, as compared to the voluntary approval process, is considered more of a formality reserved for those instances where the product is neither controversial nor presents issues requiring extensive analysis or consideration of the public interest, the latter being a determination that is properly made by the Commission.9

The Perils of Revision

As the Chairman has recently noted, “The CFTC has received some criticism from large market participants for not holding public hearings prior to self-certification of Bitcoin futures.”10 That being said, as the most recent CFTC backgrounder notes, “the product self-certification process does NOT provide for public input.”11 And narrowing focus to the two bitcoin futures contracts, the Chairman clarified, “Neither statute nor rule would have prevented CME and CFE from launching their new products before public hearings could have been called.”12 While the self-certification process does not expressly provide for public input, that does not mean that public input in the process of launching new and novel products is impossible or undesirable. To the contrary, dialogue between the Commission, the exchanges, and market participants is vital to the process. I am hopeful that today’s MRAC meeting will both shed light on the importance of such dialogue and perhaps provide the public input regarding Bitcoin futures that did not occur prior to certification. At the very least, this meeting provides a forum for public input regarding future products in the virtual currency space.

The CFTC staff developed a standard of “Heightened Review”, “within the limits and parameters of the current self-certification process, for determining whether the Bitcoin futures products comply with the exchange’s obligations under the CEA core principles and CFTC regulations and related guidance.”13 I fully support and commend the staff, under the direction of the Chairman, for taking initiative and quick action in a timely and direct manner to address concerns related to the listing of Bitcoin futures contracts despite the regulatory confines of the self-certification parameters.

However, the need for a new “Heightened Review” process demonstrates that the Commission must reconsider its historical regulatory approach to new products – in fact, the implementation of the “heightened review” process is a new regulatory approach in and of itself. Such changes require a more formal process, subject to Commission deliberation and public notice and comment. I am pleased that the Chairman has asked the CFTC’s General Counsel to propose for Commission consideration possible regulatory and/or statutory steps to better support the staff’s approach to virtual currency product review.14 I look forward to exploring our options, which I hope will include some parameters for determining when self-certification may not be appropriate, and for determining when such matters are appropriately brought before the Commission.

Self-Certification Works

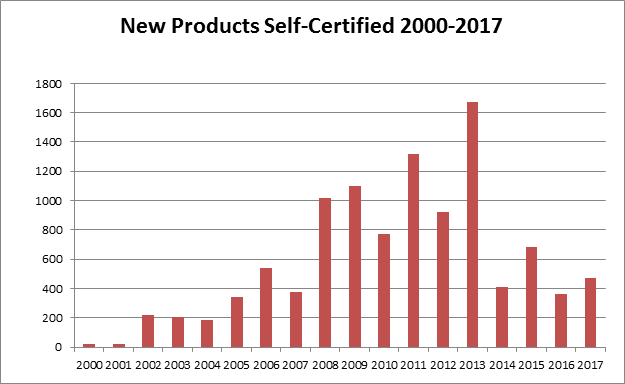

To be clear, this meeting is not intended to question the efficacy and usefulness of self-certification. Self-certification is a unique process that has served market participants, the CFTC, and the general public very well. Indeed, since Congress authorized the CFTC to establish a self-certification process for the listing of new futures products in 2000,15 exchanges have self-certified 10,628 new products, providing more risk management tools for commercial end-users across many different asset classes.16 As set forth in Part 40 of the Commission regulations, it is a process that relies on the Act and core principles as the benchmarks and standards for how an exchange and derivatives clearing organization (“DCO”) must design a product. Any action above and beyond this must be subject to Commission action so that the Commission, as a whole, may deliberate the merits and consider the risks of new products in a transparent forum.

* Data compiled from the CFTC’s Filings and Actions database, which includes submissions from DCMs, DCOs, and Swap Data Repositories (“SDRs”).17

The Agenda

Our first panel today will focus on the statutory and regulatory frameworks and processes with respect to the listing of new products through self-certification. A part of the discussion will be devoted to clarifying the different internal processes for review associated with self-certification versus voluntary approval. Of particular relevance to me is the Commission’s flexibility under each of the governing Commission rules to assure the opportunity for thoughtful analysis and public comment in appropriate circumstances.

Our second panel will focus more specifically on how the Commission assesses, initially and on an on-going basis, the adequacy of risk management and surveillance of new products. Panelists from the Commission’s Divisions of Clearing and Risk, Swap Dealer and Intermediary Oversight, and Enforcement will provide insight into how each of their Divisions considers products that present novel or unique risk profiles, and how they go about developing the expertise necessary to accomplish their missions.

Our third panel features representatives from DCMs and DCOs who will discuss the self-certification process from their perspective.

Our fourth and final panel will address the question of novelty. The experts on this panel will discuss the question of novelty and whether the current self-certification process allows for adequate regulatory consideration when a product is itself determined to be novel or presents complex or unique issues.

Closing

I am hopeful that today's conversation will serve to educate the public on the success of the self-certification process, and perhaps shed light on what lies ahead in the virtual currency space. As market participants introduce new virtual currency products in the months and years ahead, I look forward to a broader conversation by the Commission in considering what steps can be taken to better evaluate novel products in a transparent manner, and to bring together all ideas, concerns, and suggestions, to best inform the general public about our process of review. In my view, novelty is a fleeting concept, which time consumes. But, while novelty exists, it shines brightly, and must be handled with care.

I believe the CFTC must prioritize, above all else, the protection of customer property, and the promotion of safe, transparent derivatives markets. With that said, the self-certification process may not be an appropriate regulatory tool for all new products. The Commission, working in partnership with market participants, and perhaps this Committee, should continue to evaluate its regulatory and procedural approach to new product listings, considering what we do and what we do not do in that process. We will ultimately be accountable for the products listed within our jurisdiction. We own this space, and we should own it responsibly. I want to do everything in my power to support and promote innovation; however, the Commission must exercise our duties such that when we look back on the record, it shows that we took the necessary steps to fulfill our mission in a careful and deliberative manner.

Everyone in this room plays a key role in the success of the derivatives market. We all have unique and often diverse interests, responsibilities, and duties. But we also have many common interests, not the least of which is the promotion and support of healthy, safe, and transparent derivatives markets. As a regulator, I believe it is the Commission’s responsibility to hold public meetings like these to educate, introduce fresh ideas, reconcile differences, and find solutions to new challenges so that market participants and the general public, our number one constituent, feels confident that we are fulfilling our responsibilities and can hold us accountable for our actions. As a community—regulators and market participants together—it is our responsibility to have these conversations, although difficult at times, to ensure we are constantly learning from past actions, and seeking better solutions to protect the public interest. I strongly believe this approach best serves all of us in long-run as these markets continue to grow, innovate, and break barriers.

I want to again thank everyone for being here today, the MRAC Committee members, the speakers, Paul Architzel, Alicia Lewis, Commissioner Quintenz, and Chairman Giancarlo. I look forward to today's discussion.

1 CFTC, CFTC Backgrounder on Self-Certified Contracts for Bitcoin Products (Dec. 1, 2017), sheet(Dec. 1, 2017) http://www.cftc.gov/idc/groups/public/@newsroom/documents/file/bitcoin_factsheet120117.pdf; and CFTC, CFTC Backgrounder on Oversight and Approach to Virtual Currency Futures Markets (Jan. 4, 2018), http://www.cftc.gov/idc/groups/public/@newsroom/documents/file/backgrounder_virtualcurrency01.pdf.

2 CFTC Talks, Episode 20, Dec. 6, 2017, Roundtable with CFTC Leaders on Bitcoin, at http://www.cftc.gov/Media/Podcast/index.

3 CFTC, Bitcoin, http://cftc.gov/bitcoin/index.htm.

4 CEA section 5(c)(1); 7 U.S.C. 7a-2(c)(1); and 17 C.F.R. 40.2 and 40.3.

5 CEA sections 5c(c)(1) and (4)(A); 7 U.S.C. 7a-2(c)(1) and (4)(A).

6 CEA section 5c(c)(5)(B); 7 U.S.C. 7a-2(c)(5)(B).

7 17 C.F.R. 40.2(a)-(c) and 40.3(a), (c).

8 17 C.F.R. 40.2(a)(1).

9 See generally Revised Procedures for Commission Review and Approval of Applications for Contract Market Designation and Exchange Rules Relating to Contract Terms and Conditions, 62 FR 10434, 10437-8 (Mar. 7, 1997).

10 J. Christopher Giancarlo, Remarks of Chairman J. Christopher Giancarlo to the ABA Derivatives and Futures Section Conference, Naples, Florida (Jan. 18, 2018), http://www.cftc.gov/PressRoom/SpeechesTestimony/opagiancarlo34.

11 CFTC Backgrounder on Oversight and Approach to Virtual Currency Futures Markets, supra note 1, at 2.

12 J. Christopher Giancarlo, supra note 10.

13 CFTC Backgrounder on Oversight and Approach to Virtual Currency Futures Markets, supra note, at 3; and J. Christopher Giancarlo, supra note 10.

14 J. Christopher Giancarlo, supra note 10.

15 See Commodity Futures Modernization Act of 2000, Pub. L. 106-554, 114 Stat. 2763 (2000), and CEA section 5c(c)(1); 7 U.S.C. 7a-2(c)(1).

16 See CFTC, Contracts & Products, http://www.cftc.gov/IndustryOversight/ContractsProducts/index.htm.

17 The data includes 4,849 security futures products and 1,223 products (all but one in electricity) certified by Nodal Exchange in 2013.

Last Updated: January 31, 2018